The Actual Concept Of Assessment and Reassessment Proceedings Of Income Tax Act

Notice under Section 148

It may not be that uncommon for you to be served by an assessment or reassessment notice under Section 148 of the Income Tax Act. There may have been some fault in the return that you have filed or for some other matters, an assessment notice requires for you to appear before the Assessing Officer to present your case and defend it if necessary.

The ‘Notice’ under Section 148

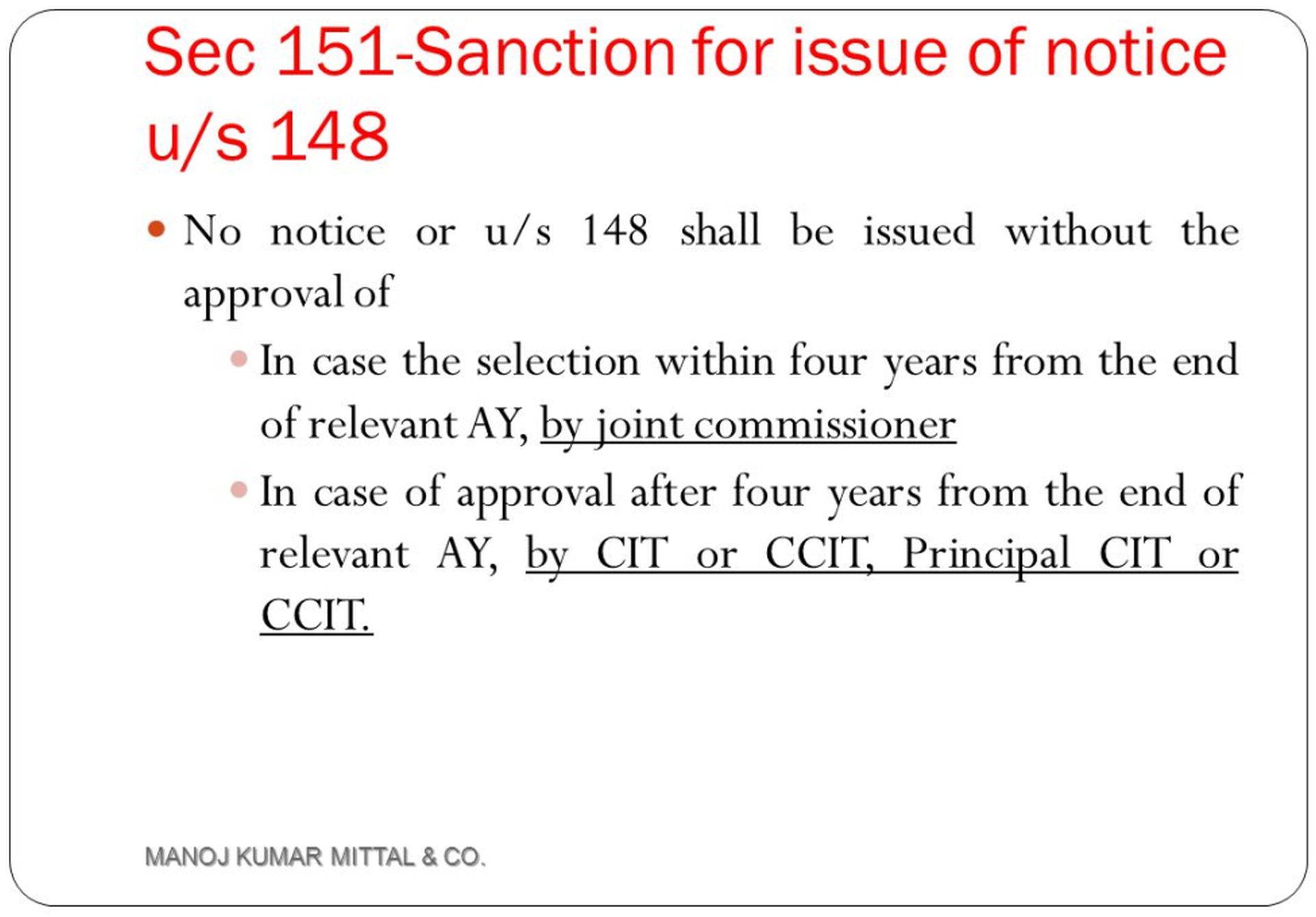

Before the Assessing Officer issues any notice, he/she must have enough reasons and evidence to believe that there are any income that is chargeable to tax, has escaped the assessment. If the Assessing Officer is confident, he/she will issue a Notice under Section 148 of the Income Tax Act to the assessee, asking him to appear before the Assessing Officer. This falls under the procedure of the reassessment as described under Section 147 of the Income Tax Act.

The issued Notice under Section 148 is essential for many a factor. This Notice serves as the authentic document issued by the Income Tax Department against any filings or court cases. So, this Notice holds an important value.

A Case Study

There are several situations, which you may face when you are served with the Notice under Section 148. One of the very particular instances has been described below, and to assist you the solution has also been provided.

Situation 1

Suppose, you have been a responsible taxpayer for several financial years and, due to some reason you have stopped paying the taxes. The reasons may include that you don’t have a job or you have relocated abroad. Now, you have received a Notice under Section 148 of the Act, but it was delivered to a wrong address and was allowed to be accepted by a family member who is not a legally authorized agent of yours.

So the question that arises is, can you send a notice to the Assessing Officer challenging the effectiveness of the service of the Notice under Section 148 and asking for reasons of sending the Notice?

Solution- If Issued Notice Under Section 148

Since the Notice under Section 148 has already been served, there is no point of challenging it. However, it is advised that when you face such situation you should file a letter to the Assessing Officer asking for reasons for reopening the assessment. When you will receive the reasons, you are at liberty to file objections before the Assessing Officer to challenge the reassessment. The AO is obligated to answer the objections raised by you. If you are not happy with the reassessment proceedings, you can always file a Writ Petition before High Court and/or appeal before CIT (A).

Delhi High Court Judgement on Provisions of Section 148 of Income Tax Act

The Delhi High Court also addressed this issue of legally authorized agent to accept the Notice under Section 148. It said that the person accepting the Notice is conscious of participating in the reassessment proceedings under Section 147, and whether he/she is the assessee or an individual who is not legally authorized by the assessee to accept such Notice, there will be no waiver of the requirement to follow the already effective reassessment proceedings under Section 147.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income