How can you get tax exemption by selling your asset under Section 54F Income Tax Conditions?

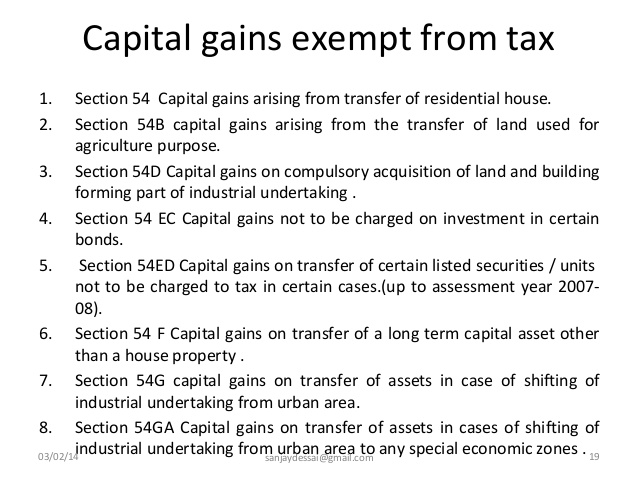

Capital Gains exempt from Income Tax

Whenever we decide to sell any long-term capital asset, the gains are large but the tax to be paid is indeed huge too. Gains on the asset held for a period longer than minimum specified period is known as Long Term Capital Gain Tax. The good news for the taxpayers in this regard is, the Income Tax Act makes it possible for claiming a relief from paying this tax. This can be done if the taxpayer reinvests the amount in certain pre-defined forms of investment. Before claiming exemption, Section 54F Income Tax Conditions have to be kept in mind.

Things to be kept in mind to claim deduction under section 54F

Under section 54, any long-term capital gain for an individual or a HUF by selling a residential property, can ask for an exemption if the capital gains are again invested in:

- Purchasing another residential property within 1 year before or 2 years after the mentioned date of transfer of the property which is sold and/or

- Constructing a residential property within 3 years of the transfer of the property.

The above terms will hold valid if the new property is not transferred within a period of 3 years, calculated from the day it was first acquired. If on the other hand the new property is sold within these three years, then the gains will be calculated by reducing the cost of acquisition of this property. The reduction will be by the amount of capital gain which is exempted according to the previous section 54.

What are the Section 54F Income Tax Conditions?

Section 54F Income Tax Conditions will help to gauge the situations better, wherein we can claim the tax exemption. Let us look at the conditions in detail:

- Capital gains acquired on the transfer of any long-term capital asset can claim for exemption if on the date of transfer of property, the owner does not have more than one residential house.

- This tax is applicable to a single residential house property in India.

- The time limit for acquiring the new asset is already mentioned above.

- For calculating the amount to be exempted the formula to be used is: Investment in new asset/Net sale consideration*capital gain. It should be always kept in mind that amount to be exempted is never more than capital gain.

- Exemption can be withdrawn if(1)the new asset is transferred within 3 years of acquisition(2)the taxpayer buys another residential property within 2 years of transfer of the previous asset in India or outside and(3)The taxpayer completes construction of another residential property within 3 years of the date of transfer, either in India or outside. This 3 year period has since been amended to 2 year vide finance Act 2017

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income