Amendments to Provisions of Tax Audit and provisions with respect to maintenance books of account

Amendments to Provisions of Tax Audit

A person is liable to get his books and accounts audited U/s 44AB (Tax Audit) by a practicing Chartered Accountant, if in the previous financial year-

- The concerned Person is carrying out any business and the Gross Total Turnover (Sales) exceeds Rs. 100 lakhs (1 Crore) or

- The concerned Person is carrying out any Profession and the Gross Receipts from his profession exceed Rs. 50 Lakhs (Applicable for FY 16-17 onwards) or

- The concerned Person is carrying out business or profession and he is covered under the preventive taxation regime under the provisions of section 44AD, 44ADA, 44AE, 44AF, 44BB or 44BBB and the declared income is lower than the deemed income computed under the relevant sections.

However, it is suggested that the threshold limit (Rs.100 lacs for business and Rs.25 lacs for the profession) may be revised to 2 crores for assessees carrying on business and to rupees 1 crore for assessees carrying on a profession.

The Due Date of e-filing the Tax Audit Report U/s 44AB is 30th September for the assessee’s who are liable for Tax Audit U/s 44AB.

Numerous modifications in Tax Audit Report have been introduced with the Income Tax (7th Amendment) Rules 2014. The Central Board of Direct Taxes has amended the tax audit forms (3CA, 3CB & 3CD forms. Apart from that, the amended forms will require explicit mentioning of observations/qualifications if any, by the Chartered Accountant while issuing the audit report.

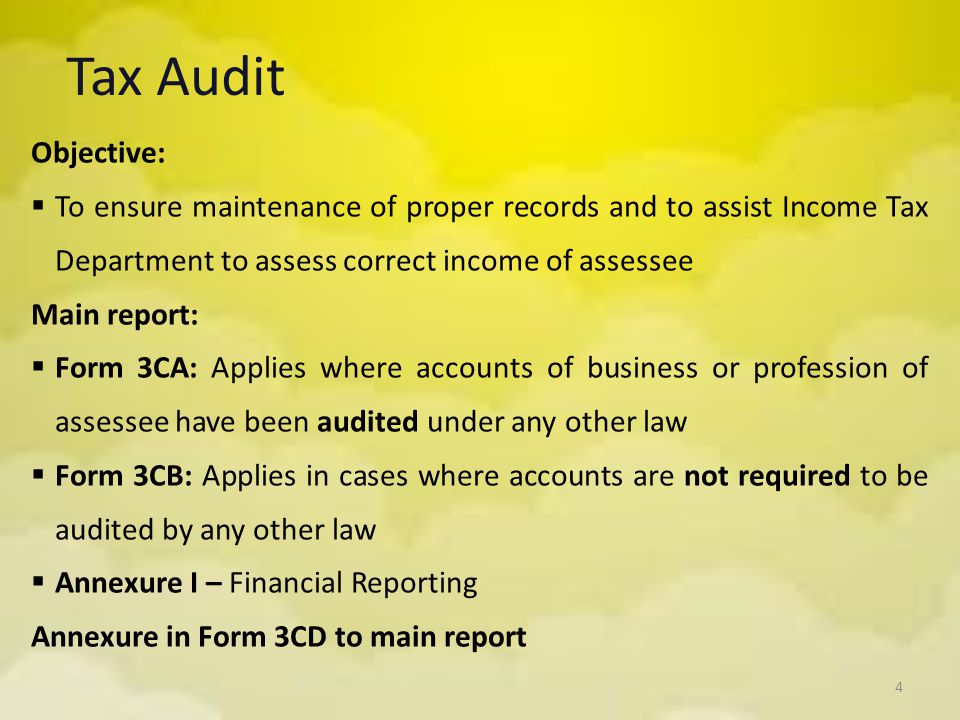

According to Rule 6G, the tax audit report is to be filed in Forms 3CA & 3CB and the particulars are required to be furnished together with these tax audit reports in Form 3CD.

- Form 3CA & Form 3CD-

Form 3CA and Form 3CD are used in the case where the Books of Accounts of-of the assessee in regard to his business have already been audited under any other Law.

- Form 3CB & Form 3CD–

Form 3CB and Form 3CD are used, where the books of Accounts of the business or profession of the assessee have not been previously audited.

Computation of Gross Total Turnover under 44AB

- Where an assessee is carrying on multiple Businesses or multiple Professions then the total turnover or receipts of both the businesses and profession shall be clubbed together. The assessee shall be liable to Tax Audit U/s 44AB if the Total Turnover/receipts exceed Rs.100 lacs ( 1 Crore) / Rs. 25 Lakhs as the case may be.

- Where an assessee is carrying on any profession as well as business and the Gross total Receipts of the aforesaid profession is Rs 22 Lakhs and the gross total Turnover of the business is Rs. 120 lacs then the assessee is liable to get his books of account audited under 44AB for both the business as well as profession. As his Gross turnover from the business exceeds the prescribed the limit of Rs. 100 lacs. However, if the Total Turnover from the business supposed to be Rs. 95 Lakhs and the Gross Receipts from the profession are Rs. 22 Lakhs, then the assessee would not be required to get his books of accounts audited U/s 44AB.

- Where an assessee has a gross total turnover of Rs. 98 lacs and sold a Car for Rs. 10 Lacs. In such a situation, the total amount would be Rs. 1.08 Lacs i.e. above Rs. 1 Crore.

However, ICAI has clarified that the gross total turnover will not consist any amount on the sale of any fixed asset as the asset was not held for the purpose of sale but for the business use.

Under the present provisions of section 44AA, an assessee carrying out business or profession is required to maintain books of accounts if, the total turnover of the assessee in any of the 3 years preceding the previous financial year is more than Rs 10 lakhs or the income of the assessee is more than Rs 1.2 lacs. Furthermore, where an assessee opting for presumptive taxation and declares his income to be lower than the specified amount therein are also required to maintain books of accounts.

Penalty for noncompliance with Section 44AB

Non-compliance with the provisions of the section 44AB shall attract Penalty U/s 271B IT Act. If any assessee is required to get his books of account audited U/s 44AB and fails to do so before the specified due date shall be liable for the penalty of ½% of the gross total turnover of the business or the gross total receipts from the profession subject to a maximum penalty of Rs. 1,50,000.

However, the penalty can be waived off if there is a justifiable cause for such failure.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income