What is The Reverse Charge Mechanism under Goods and Service Tax (GST)?

Reverse Charge Mechanism under Goods and Service Tax

A revolutionary change has been brought about the entire taxation system of India, with the onset of a new tax structure named Goods and Service Tax (GST). VAT, CST, Excise Duty, Service Tax and 13 other taxes along with 22 Cess taxes have been subsumed under one tax i.e. Goods and Service Tax. Quite a number of people are confused about the new tax revolution that has changed the entire indirect taxation part of the country overnight, many are still trying to figure out what exactly GST is and how previously being charged taxes will be incorporated in it and how will they be applicable from now onwards.

Understanding the term Reverse Charge under Goods and Services Tax

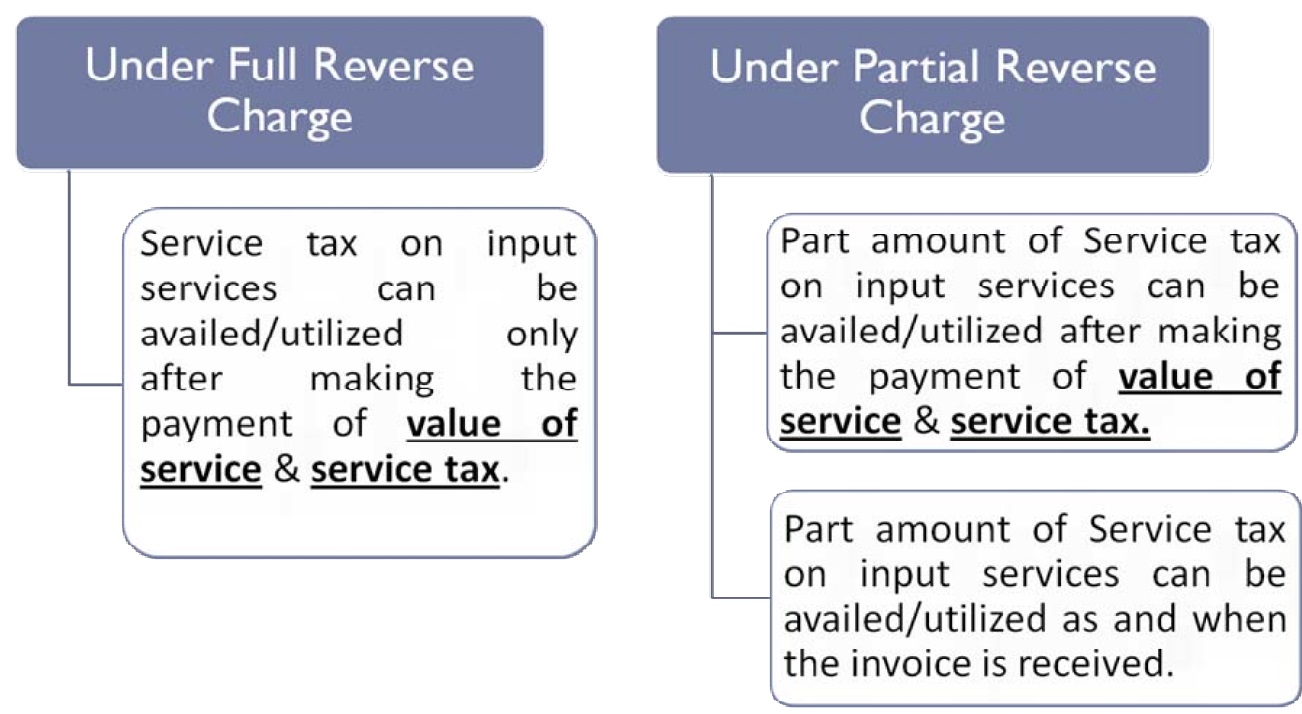

Previously service tax was charged @ 15% (14% Service tax, 0.5% Krishi Kalyan Cess and 0.5% Swach Bharat Cess) on the supply of goods and services, except on those mentioned in the negative list. Service tax was collected by the service provider and paid to the central government but there were five exceptional cases where service tax is liable to be paid by the service receiver and not the service provider. Since the charge of payment of service tax is reversed in five cases that is why the term was given “Reverse Charge”. Reverse Charge was defined under Section 2(98) of the Service Tax Act.

Applicability of Reverse Charge Mechanism under CGST

Previously reverse charge was applicable on five cases where the service recipient was liable to pay service tax. But under Section 9 (3) of the CGST Act, 2017, the government decided on 19th may 2017 to include eighteen types of services where the reverse charge mechanism is applicable. In the case of goods, the government hasn’t come up with any such list yet. Section 9 (4) of the CGST Act, 2017 further states that if a recipient of goods and services or both is registered under the GST Act and receives the services from an unregistered service provider of goods and services or both then, in this case, the service recipient is liable to pay service tax.

Applicability of Reverse Charge Mechanism under IGST

Under Section 5 (3) of the IGST Act, 2017, the government clarified that the government may specify categories of goods and services or both on which the reverse charge mechanism is or will be applicable. Section 5 (4) of the IGST Act,2017, states that integrated tax on supply of goods and services from a person who is not registered under the GST Act is received by a person registered under the GST Act, then reverse charge mechanism will apply.

Relevant Documentation Requirement for complying with Reverse Charge Mechanism under GST

A person who is required to pay service tax under the reverse charge case is required to issue an invoice in respect of goods and services received by him to the service provider who is not registered under the GST Act, 2017. The invoice is required to be given on the date of receipt of goods or services or both. Apart from issuing an invoice, the service recipient is also required to issue a payment voucher to the service provider on the date of payment to the supplier of goods or services or both.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income