What is remedy to taxpayer if the Tax deductor fails to deposit the TDS or fails to file TDS Return

Consequences of TDS not deposited by Deductor

Repercussions of a Tax Deductor Not Depositing TDS with the Government in India

In India, when a tax deductor (typically your employer/ Principal who awarded the Works Contract) deducts Tax at Source (TDS) from your salary/ Professional Payments or income but fails to deposit it with the government, it creates a situation with several consequences:

For the Employee/Taxpayer (You):

Loss of Tax Credit:

You won’t be able to claim the deducted TDS amount as a tax credit when filing your Income Tax Return (ITR). This can potentially lead to higher tax liability.

Tax Demand Notice:

If you claim the Tax deducted in your ITR and such tax wasn’t deposited by deductor, you will receive a tax demand notice from the Income Tax Department due to a mismatch in the records.

Caught Between Authorities:

You might get stuck in a situation where you may have to deal with both the Income Tax Department and your employer to resolve the issue.

For the Tax Deductor (Employer):

Penalties and Interest:

The employer will face penalties and late payment interest charges for not depositing the TDS on time.

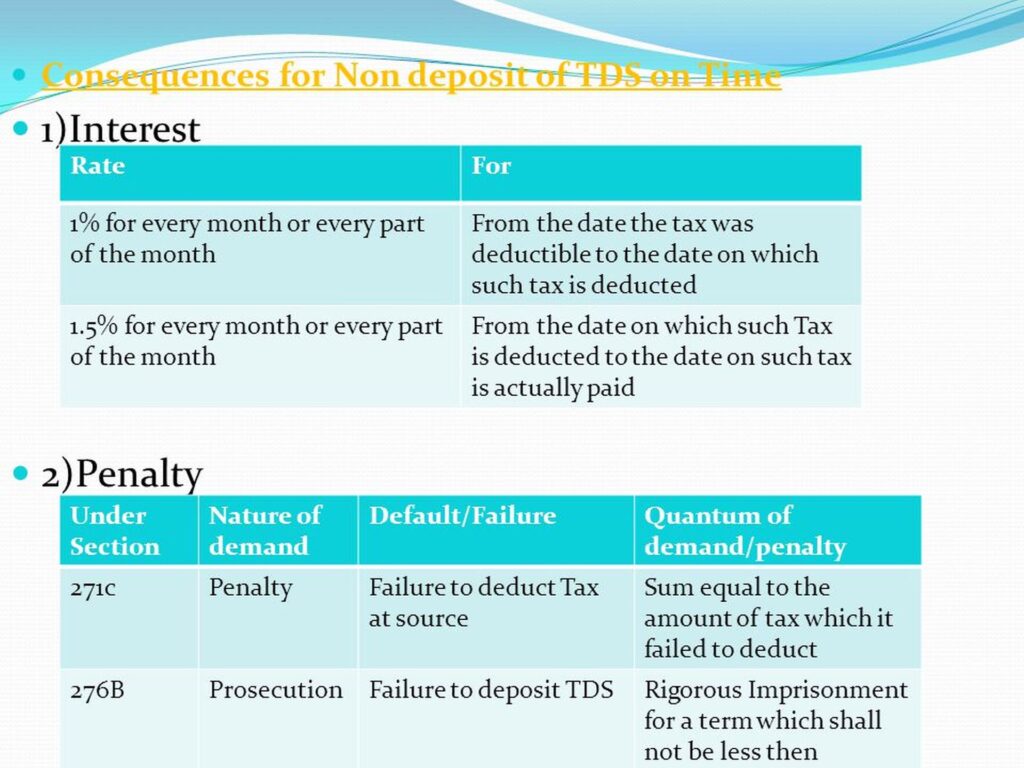

Some major interest and penalties payable by deductor would be-

- Penalty u/s 201A for Non-deduction of TDS, either in whole or part. This penalty is levied @ 1% per month From the date on which the tax was to be deducted to the actual date of deduction

- Penalty u/s 201A for Non-payment of TDS (after deduction) and this penalty is [email protected]% per month from the date of deduction to date of actual payment

- Prosecution u/s 276B for failure to deposit TDS which can lead to rigorous imprisonment.

Remember: The employer/ deductor cannot recover these penalties from your salary/ Contract payments. The onus of depositing TDS and complying with tax regulations lies solely with the deductor.

Disallowance of Expenses: In some cases, the Income Tax Department might disallow the employer to claim the deducted TDS amount as a business expense. This can lead to higher tax liability for the employer.

Difficulties in Obtaining Tax Clearance Certificate (TCC): A Tax Clearance Certificate (TCC) is often required for various purposes like participating in government tenders or applying for loans. Non-deposition of TDS can hinder the employer’s ability to obtain a TCC, potentially impacting their business operations.

Here’s what you can do if your employer / deductor hasn’t deposited your TDS:

Check Form 26AS:

This is your tax credit statement generated by Income Tax Department and gets compiled based on various TDS deductions made and accordingly TDS returns filed by various deductors. Regularly verify your Form 26AS to ensure the TDS deducted reflects accurately.

Inform your Employer/Deductor:

Bring the discrepancy to your employer’s attention and request them to rectify the situation by depositing the TDS with the government.

File Compliant with Income Tax Department with full relevant details:

If the employer doesn’t address the issue, you can still file your ITR. While, at the time of filing the income tax return, you do not have any provision to share any supporting document, it will be good idea to file grievance with Income Tax department. While filing grievance you can attach any supporting document in support of your complaint. In this grievance you can explain the TDS claimed and the mismatch in Form 26 due to non deposit of TDS by deductor.

Please note that the Income Tax Department cannot penalize the employee for the employer’s mistake of not depositing TDS. Please note filing the complaint with Income Tax Department against the deductor would always be handy in case where deductor refuses to rectify the issue by depositing TDS or by filing the TDS return as the case may be.

What if the Income Tax Department still does not allow credit of TDS deducted and proceeds to raise demand against you?

This is not an unlikely event and, in many cases, Income Tax Department can raise the department till deductor does not deposit TRDS and files TDS return.

If so happens, don’t worry and here are some landmark cases in India that support the assessee’s (taxpayer’s) rights when the deductor (employer) fails to deposit TDS with the government:

Kiran S Patel vs. Adit, Cpc, Bengaluru (2022): This case from the Karnataka High Court highlights that the assessee cannot be denied credit for TDS even if the employer hasn’t deposited it. The court emphasized Section 205 of the Income Tax Act, which states that the assessee shouldn’t be asked to pay tax again if TDS has been deducted.

Anusuya Alva vs. DCIT (2005): The Karnataka High Court ruled in this case that if the deductor deducts tax from rent but doesn’t deposit it, the tax department can only recover the amount from the deductor, not the assessee.

CBDT Clarifications: The Central Board of Direct Taxes (CBDT) has issued instructions acknowledging this issue. They clarify that the assessing officer cannot raise tax demands on the assessee if the deductor fails to deposit the deducted TDS.

Here are some additional cases that reinforce the assessee’s rights when the deductor fails to deposit TDS:

Shalini Garg vs. ACIT (2017): The Delhi High Court reiterated the principle established in the Kiran S Patel case. The court ruled that the assessee cannot be penalized for the deductor’s inaction of not depositing TDS. The court emphasized that the assessee has fulfilled their tax obligation by paying the deducted amount at source.

Pratibha Goyal vs. ITO (2014): The Income Tax Appellate Tribunal (ITAT) ruled in this case that the assessee is entitled to tax credit for TDS deducted from her interest income, even though the bank (the deductor) failed to deposit it with the government.

Commissioner of Income Tax vs. Vindhya Telelinks Ltd. (2010): The Supreme Court of India, in this case, clarified the distinction between deduction of tax and deposit of tax. The court ruled that deduction of tax at source by the deductor is a separate event from the subsequent deposit with the government. This distinction protects the assessee from being held liable for the deductor’s non-compliance.

ITAT Rulings: The Income Tax Appellate Tribunal (ITAT) plays a crucial role in resolving tax disputes. Numerous ITAT rulings reiterate the assessee’s right to claim tax credit for deducted TDS, even if not deposited by the deductor. These rulings provide further support for taxpayers facing such situations.

CBDT Circulars: The Central Board of Direct Taxes (CBDT) issues official circulars to clarify tax-related issues. While not legally binding judgments, these circulars often acknowledge the assessee’s rights regarding non-deposited TDS by the deductor. These pronouncements by the tax authorities offer additional backing for taxpayers.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income