FAQ on Cash Receipt of Rs.2 Lakh or More w.e.f 1.04.2017 (Section 269ST)

Section 269 ST has been introduced in this budget, which has draconian provisions. However would these provisions be strong enough to deter a tax evader to go cashless and use banking channels instead

In next article we will soon cover how these provisions can be made mockery of by scrupulous tax evader

| S No | Questions | Answers |

| 1) | From which date this section is Applicable | This section applies from 01/04/2017 (F.Y.2017-18 Onwards) |

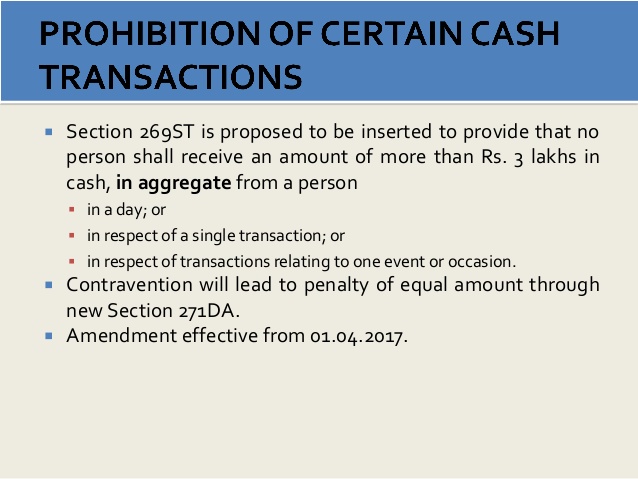

| 2) | What are the provisions of Section 269 ST | Finance Bill 2017 proposed to insert section 269ST in

the Income Tax Act to provide that no person shall receive an amount of Two lakh rupees or more,— (a) in aggregate from a person in a day; (b) in respect of a single transaction; or (c) in respect of transactions relating to one event or occasion from a person, other-wise than by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account |

| 3) EXAMPLES OF TRANSACTIONS COVERED IN (a), (b) & (c ) above | ||

| (a) in aggregate from a person in

a day |

E.g. if a person receives Rs.2.25 lakhs in cash for 2 different bills of Rs.1 lakh and 1.25 lakh, then also penalty is levied | |

| (b) in respect of single

transaction |

E.g. if there is single bill of Rs.3.10 Lakh and cash is received on different days of Rs.1.6 lakh and Rs.1.5 lakh, then also penalty is levied. | |

| (c) in respect of transactions relating to one event or occasion from a person | E.g. if marriage is one occasion and a person

receives amount of Rs.3,00,000/-. Thus penalty is levied of 100% of amount received. |

|

| (d) withdrawal of amount from own bank account | E.g. if a person withdraws in a day amount of Rs.2 lakhs or above, then penalty is levied. | |

| 4) | To whom does Section 269 ST

applies? |

To any person receiving cash above Rs.2 lakh |

| 5) | For which transactions is Section 269ST not applicable? | Restriction on cash receipt of Rs.2 Lakh or more w.e.f

01.04.2017 shall not apply to Government, any banking company, post office savings bank or co-operative bank. Transactions of the nature referred to in section 269SS; Such other persons or class of persons or receipts, as may be specified by the Central Government by notification in the Official Gazette. |

| 6) | Whether penalty is applicable for regular receipts only? | Any type of amount of Rs.2 Lakh or above received in cash whether capital or revenue in nature. |

| 7) | Whether exempt income is covered under Section 269ST? | Both taxable and exempt incomes are covered in Section 269ST. |

| 8) | If the amount is received for

personal purpose, whether 269ST is applicable? |

Irrespective of purpose of accepting amount i.e., whether business purpose or personal purpose or as a trustee, custodian etc. section 269ST is applicable. |

| 9) | What is the Penalty for

Contravention of Section 269ST? |

100% penalty on receiver of amount. |

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income