Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?

Lapsed LIC Insurance Policies

Lapsed LIC Insurance Policies – If there a way out?

If the insurance premium of a policy is not paid within the specified date (including grace period) the policy lapses. The revival of the lapsed policy is a fresh agreement where the insurer can impose fresh terms and conditions. The Lapsed LIC Insurance Policies due to non-payment of premium can be revived within two years period from the date of elapsing of the policy by paying arrears of interest and premium together with the fulfillment of medical requirements if any.

The revival of the Lapsed LIC Insurance Policies can be done under the following categories:

- Ordinary Revival

- Revival on non-medical basis

- Revival on medical basis

- The other schemes for revival are:

- Survival Benefit- cum- revival

- Revival by installment

- Loan- cum- revival

- Special Revival Scheme

The Money back limit and specified cases

The percentage of LIC policy that lapse every year stands around 4 percent on an average of last three years. The insurance premiums that received within the lapsed LIC policies become the overall part of the Life Fund.

Where the premium is paid for less than THREE years for the policy which has premium paying term of TEN years or more, then the policy stand lapsed. Similarly, where the premium is paid for less than TWO years for the policy with a premium paying term of fewer than TEN years, then the policy stand lapsed.

Can you have Guaranteed Surrender Value?However, as per provisions contained in the Regulation 35 of the IRDA (Non-Linked Insurance Product) Regulations 2013, they acquire guaranteed surrendered value only if the premium is paid for 3 consecutive years at least with premium paying term of 10 years or more and similarly, if the premium is paid for two consecutive years with a policy of Premium Paying Term of less than TEN years.

The provisions contained in the Regulation 35(f) of the IRDA (Non-Linked Insurance Product) Regulations 2013, states that the policies which have acquired a surrender value shall not be lapsed by the reason of the failure to pay further premiums but shall remain alive to the level of the paid-up sum insured. The provisions contained in the IRDA (Acquisition of Surrender and Paid UpValues) Regulations, 2015 states formula for the surrender value calculation and norms for arriving at the paid up value.11

Related Read- Is Insurance Policy a Good Investment?

Life Insurance Policy Payouts – Are they Taxable or Not?

Life Insurance Policy Payouts – Are they Taxable or Not?  Insurance is a Practical Business Investment

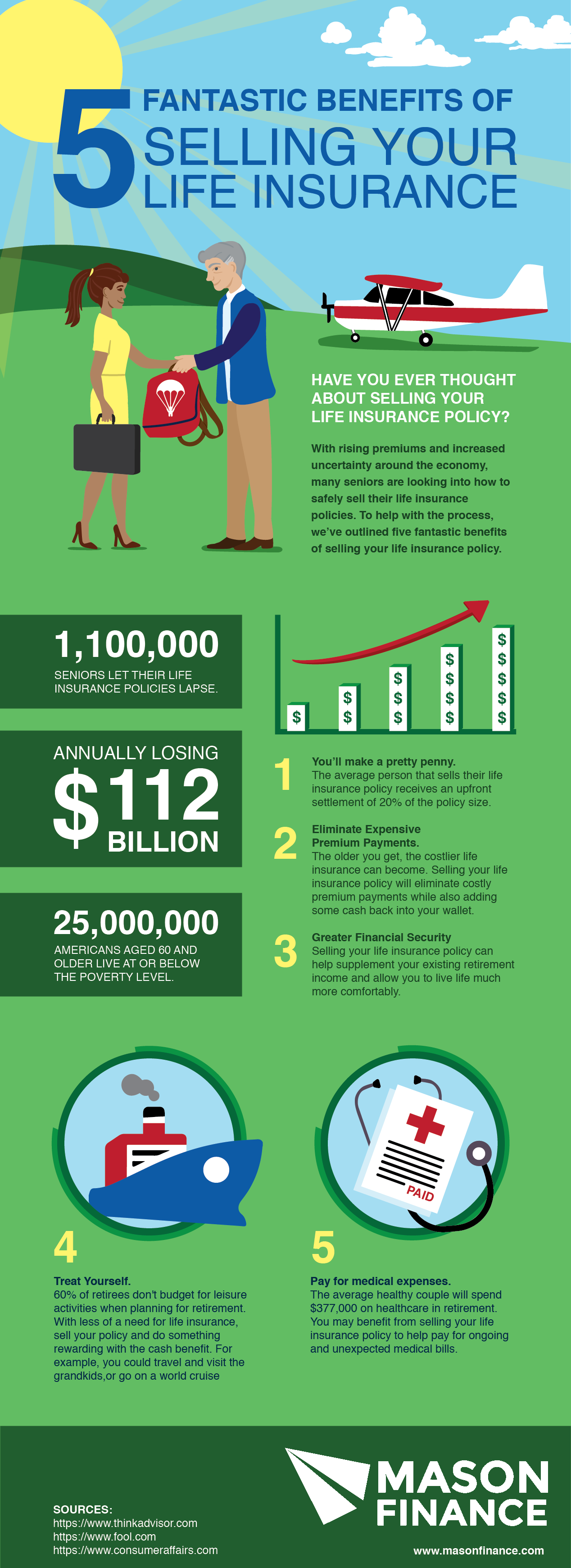

Insurance is a Practical Business Investment  5 fantastic benefits of selling your life insurance

5 fantastic benefits of selling your life insurance  Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you

Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you  Life Insurance Policies – Are they really bliss?

Life Insurance Policies – Are they really bliss?  What Insurance Companies do not tell you before selling Endowment Policies

What Insurance Companies do not tell you before selling Endowment Policies  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?