Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you

insurance plans words in the middle of many colored doors illustrating the several confusing options for you to compare and decide which policy and coverage is best for you

You are wrong if you think that all your life insurance needs are covered with an accidental death and dismemberment (AD&D) policy. There is a huge difference between Term life insurance and accidental death and dismemberment insurance policies. You should know the difference between the two before buying any policy.

Term life insurance

Term life insurance is a type of life insurance policy in which death benefit will be paid to the beneficiary if dies within a specific time period regardless of the cause of death. You choose the amount of coverage and the policy term ahead of time, and your payments and benefit amount are guaranteed to stay the same.

Term lengths typically range from 10 to 30 years. If you die after the term ends, there’s no payout because the policy has expired. You can renew or purchase a new policy at the end of your term, but your life insurance rates will be higher than before because you’ll be older and more at risk of dying.

Accidental death and dismemberment

In Accidental death and dismemberment policy, you receive benefit only if you die or get injured only from an accident. If you are killed by any reason other than an accident, there will be no pay out.

To qualify for a payout for injury, you must lose a body part or the ability to hear, see or speak. If you die in an accident covered by AD&D, your beneficiaries receive the full payout. If you suffer an injury, the policy generally pays out only part of the benefit.

Advantages of AD&D

If you die in an accident or become permanently disabled, your dependents will face a financial crisis as there would be no monthly income and the expenditure would increase.

Hence it is important to purchase an AD&D Policy as it has the following advantages-

• Family security

• No requirement of medical tests and documentation

• Substantial cover at lower premium

• Can be bought for individually or family

• Easy and certified claim process

• Legal and funeral expenses

• Child education advantage

• Highly customized plan

Limitations of AD&D

AD&D has various disadvantages also as compared to the term life insurance which are listed below-

First, as AD&D policies have very narrow risk coverage, it may not be a better option than term life insurance.

Second, your chances of dying in an accident are relatively less. A lot more people die due to various health diseases like cancer, heart attack, etc. and AD&D Policies do not provide any benefit in these cases.

Third, it must be proved that a death or injury was directly caused by a qualifying accident or within a certain time frame after it occurred, usually three months.

Fourth, AD&D policies do not cover various high risk activities such as car racing or skydiving. Also, if the insured die due to drug overdose, mental illness, drunken driving etc. no benefit would be provided.

Which is right for you?

Although you’ll pay higher premiums for term life, term life insurance is a better option because it provides more coverage and, often, the chance for a higher payout for your loved ones. If it’s very likely that you’ll die or get injured due to an accident, than only AD&D policy may be a good idea, although you may have a higher premium if you’re at high-risk because of your occupation or activities.

Life Insurance Policy Payouts – Are they Taxable or Not?

Life Insurance Policy Payouts – Are they Taxable or Not?  Insurance is a Practical Business Investment

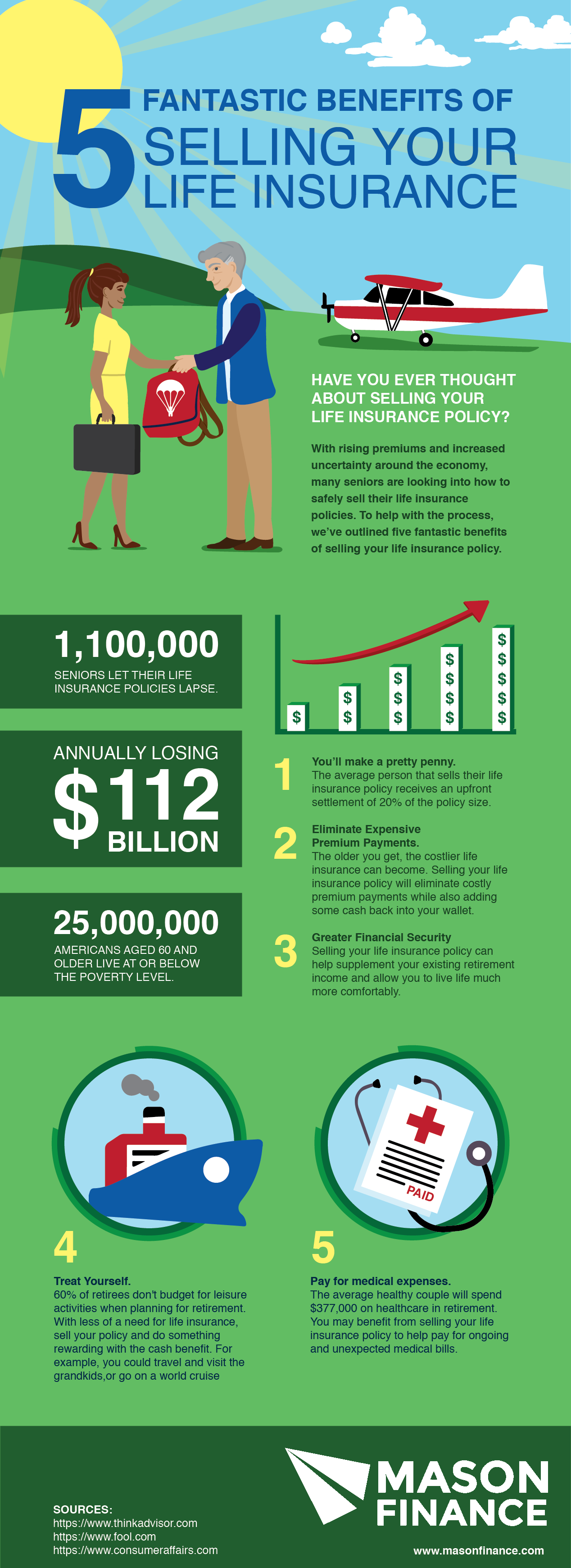

Insurance is a Practical Business Investment  5 fantastic benefits of selling your life insurance

5 fantastic benefits of selling your life insurance  Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?

Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?  Life Insurance Policies – Are they really bliss?

Life Insurance Policies – Are they really bliss?  What Insurance Companies do not tell you before selling Endowment Policies

What Insurance Companies do not tell you before selling Endowment Policies  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?