Reality of the tax-saving lucrative plans offered by the wealth Managers and the Bank Executives

These days’ lots of Insurance companies are coming up with lucrative plans to attract the people. People, on the other hand, look for the plans which can provide them with the maximum benefit it can. Stay tune to see the Reality of the tax-saving lucrative plans.

The Reality of the tax-saving lucrative plans

How about the plan that provides a tax-saving option, tax –free income at regular intervals and lump sum amount on maturity?

Sounds Great? What if in addition to the above benefit, you also get the life cover? At the age of 35, you start Investing Rs 65000 every year for 20 years, and you will get the money back of Rs 1.5 lakh in four Installments at the end of fourth, eighth, twelfth and sixteenth years. An aggregate amount of Rs 5 Lakhs on the maturity of 20 years, a simple reversionary bonus of about Rs 3.8 lakh besides the guaranteed payment. In case you die during the term of the plan, your nominee will get Rs 10 lakh. What more do you want? The plan seems to be the ideal one.

However, in reality, these lucrative plans offered by the big Insurance Companies earned very low Internal Rate of Return (IRR) which is 2.23%. It’s even less than what a saving bank offers. On the contrary, the Insurance Companies argues that the plan covers the Life of a person, and hence the returns get impacted.

Plans promise you High Return but in Reality returns are Decidedly Less-

Even though the returns are decidedly less, the insurance companies can attract investor during the tax planning season. Lakhs of money-back policies and endowment plans are sold every year. This is because most of the investor doesn’t have the time or propensity to go into the details of the policy. To get over quickly with the investment proof deadline given by their employers’ investors take the plan as framed by the salesperson of the Insurance Company. As a result, lots of complaints are against the Insurance Company.

One should Protect oneself from the Trap of Bank Executives and Insurance Companies-

To pool a large number of investors- the wealth managers and bank executives use various tricks. One can avoid getting trapped by educating or updating himself or herself.

Following things we need to know:

- Even if any plan is like ELSS and cover Life insurance, it should be noted that it is nothing but Ulip and the life cover is not free. Ulips are not flexible like ELSS funds. The early surrender charges are very high, and it has a lock-in period of 5 years.

- There are insurance companies who take the help of banks to attract customers. Usually, PSUs bank enjoys a lot of trust among their customers. To make the policy appear lucrative and reliable the distributor projects it as a scheme from the bank.

- It should be noted that the plan which is just like an FD, gives tax-free returns and cover insurance is nothing but the endowment insurance policy. It offers little returns, requires a multiyear premium commitment and have very high surrender charges.

- Pension plans offered by the Insurance companies have much higher charges as compared to the low-cost NPS(National Pension System). It’s been almost ten years since the pension scheme is open for the general public, but wealth managers and relationship managers in banks have little knowledge on it. Moreover, nobody wants to promote low-cost NPS. Instead, Bank executives encourage pension plans from insurance companies.

- ELSS funds are linked to market and are subject to market risk hence it is not advisable to invest large amount at a time. There is a lock-in period of 3 years. Best thing to do is to start SIP in ELSS fund at the starting of the financial year.

No Doubt, investing in ELSS fund is one of the best ways to save tax. An Assessee can create wealth by investing in these equity funds apart from saving tax under sec 80c.

How Budget 2020 Made the Dividend Option of Mutual Funds Tax Inefficient?

How Budget 2020 Made the Dividend Option of Mutual Funds Tax Inefficient?  HUF- a tax planning tool to save Income tax

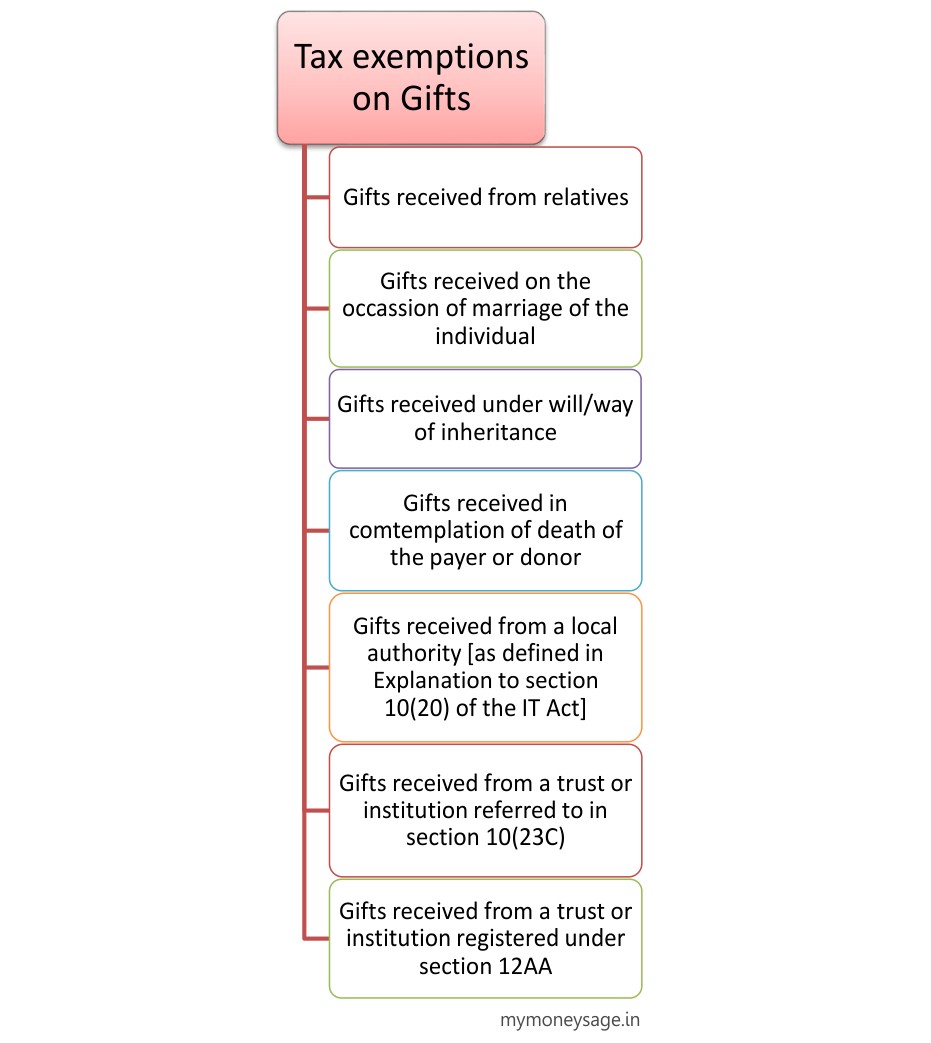

HUF- a tax planning tool to save Income tax  Do I owe a tax for the gift I receive? Get to Know the Rules of Taxability of Gift in India

Do I owe a tax for the gift I receive? Get to Know the Rules of Taxability of Gift in India  Restructuring your Salary in Tax Efficient Manner can increase your carry home Salary by upto 10%

Restructuring your Salary in Tax Efficient Manner can increase your carry home Salary by upto 10%  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?