New House is in wife’s Name – Forget about tax-relief from the sale of the house

New House is in wife’s Name - Forget about tax-relief from the sale of the house

In a recent case, Mr. R Gavankar sold a house which was jointly owned by him and his wife. He refuses to pay the tax on capital gains. It was assessed by the I.T Authorities, and they found that 50% of the LTCG of Rs 17.5 lakh is in his hands. He claimed for the deduction under sec 54, but it was denied. It was held by the Lower tax authorities, including commissioner of IT (appeals), that to get the benefits under this section, the taxpayer must own or have the legal title of the new property. Let’s know more about New House is in wife’s Name – Forget about tax-relief from the sale of the house.

Thinking of Buying New House is in wife’s Name – Forget about tax-relief from the sale of the house

Mr. R.Gavankar claimed before ITAT that sec 54 is a beneficial provision and he should get the I-T benefit available to him.

To avail tax – relief from capital gains under Section 54 of the IT Act, the sale proceeds of the old house should be used to acquire a new property within two years from the sale date of the old house. There could be various reasons for selling the property like job transfers, retirement, etc.

The Mumbai Bench of Income-Tax Appellate Tribunal (ITAT)’s denied the benefit to be sought from sec- 54 of the Income-tax Act. The reason behind this denial was that the new house bought by the taxpayer was not in his name but in the name of his wife and his adult daughter.

However, in a case similar to this, the Delhi High court gave a favorable view to the taxpayer. Bound by the decision of the Bombay High Court, ITATs Mumbai bench took a contradictory opinion and held that the taxpayer must have the legal title of the new property. The tax-payers who come under the jurisdiction of the Bombay HC must be aware of this to avoid any tax litigation.

In case the tax-payer wants to register the new residential property in his her spouse name or children’s name, it would be advisable to add his or her name to it. As per Puneet Gupta, director, People Advisory Services at EY-India, if the tax-payer name is added, at least a proportionate deduction would be available to the tax-payer (say, one-third of the cost of the new house if the taxpayer name is registered jointly with the names of a spouse and a child).

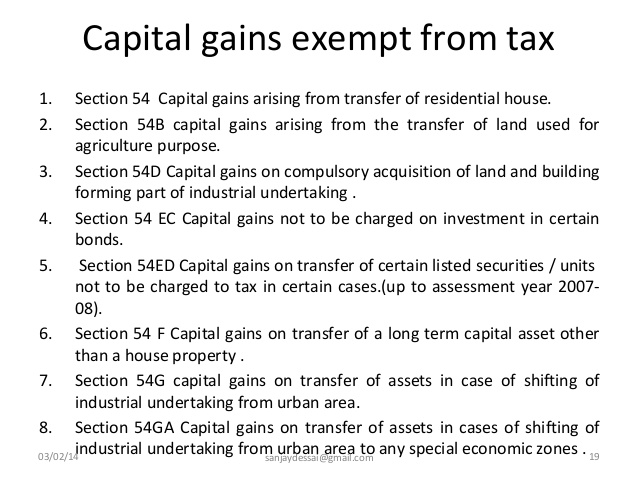

Under Sec 54 of the IT Act, to avail tax relief one should invest the long-term capital gains from the sale of an old house in a new house within two years from the sale date. The profit earned from the sale of a residential property held for two years is treated as long-term capital gain (LTCG). Such gain is taxable at 20% with adjustment for inflation which is termed as indexation benefit.

If the taxpayer within the stipulated period invests the earned capital gain in the purchase of a new house, the tax on the LTCG will get reduced to the extent of investment in the new house. The stipulated period to invest the LTCG is two years from the sale date of the old house. The taxpayer can also avail tax benefit if he constructs a new residential house within three years of the old house’s sale.

Note: The whole transaction of selling and buying must be in India to avail tax benefit under Sec 54 of the IT Act.

Tax Implications by Owning Residential Property by an NRI in India

Tax Implications by Owning Residential Property by an NRI in India  How can you get tax exemption by selling your asset under Section 54F Income Tax Conditions?

How can you get tax exemption by selling your asset under Section 54F Income Tax Conditions?  Section 80IBA Assures 100% Deduction For Affordable Housing Projects

Section 80IBA Assures 100% Deduction For Affordable Housing Projects  How to Minimize Tax Liability with House Rent Allowance

How to Minimize Tax Liability with House Rent Allowance  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?