ICDS may result in penalties for companies and may result in more disputes

APPLICIABILITY:

The Central Government hereby notifies the income computation and disclosure standards as specified in the Annexure to be followed by all assessees, following the mercantile system of accounting, for the purposes of computation of income chargeable to income-tax under the head “Profit and gains of business or profession” or “ Income from other sources”.

EFFECTIVE FROM:

Effect from 1st day of April, 2015, and shall accordingly apply to the assessment year 2016-17 and subsequent assessment years.

| ICDS NO. | ICDS NAME | AS NO. |

| I | Accounting Policies | 1 |

| II | Valuation of inventories | 2 |

| III | Construction contracts | 7 |

| IV | Revenue recognition | 9 |

| V | Tangible fixed assets | 10 |

| VI | The effects of changes in foreign exchange rates | 11 |

| VII | Government grants | 12 |

| VIII | Securities | 13 |

| IX | Borrowing costs | 16 |

| X | Provisions, contingent liabilities and contingent assets | 29 |

ICDS v/s AS:

ICDS II: ICDS provide for valuation of inventory for service providers, which is specifically excluded from AS 2. The inventory in such cases would include contracts in progress on the last day of the year but not those that have been completed.

ICDS III & IV: Revenue from construction contracts and service contracts must be recognized by a percentage completion method.

ICDS VI: Treatment of premium/discount on forward contracts will be governed by the provisions of ICDS, which appear to differ from existing court judgments.

ICDS VII: All kinds of government grants would now become taxable, either upfront, or by way of reduced depreciation.

ICDS IX: Borrowing costs must be capitalized according to a special formula provided under the ICDS. This formula is different from the concept of Weighted Average Cost of Borrowing specified under AS 16. Also, all fixed assets are considered as ‘Qualifying Assets’.

VIEWS:

Although the government has clarified that wherever the ICDS contradicts the I-T Act the latter shall prevail, There are many chances of disputes which may result in huge penalties.

“While we expect more clarity to emerge from the CBDT, it is quite likely that wherever a Supreme Court judgment has interpreted the provisions of the Income Tax Act, it would prevail over ICDS but in cases where the judicial pronouncement is based on an interpretation of the boarder commercial or accounting principles, the requirements of the ICDS may prevail,” said Sai Venkateshwaran, partner and head of accounting advisory services at KPMG.

Conclusion:

There should be more clarification on ICDS, They should be amended and they should be in align with Tax Provisions, so that there will be no disputes.

Tax Implications by Owning Residential Property by an NRI in India

Tax Implications by Owning Residential Property by an NRI in India  New House is in wife’s Name – Forget about tax-relief from the sale of the house

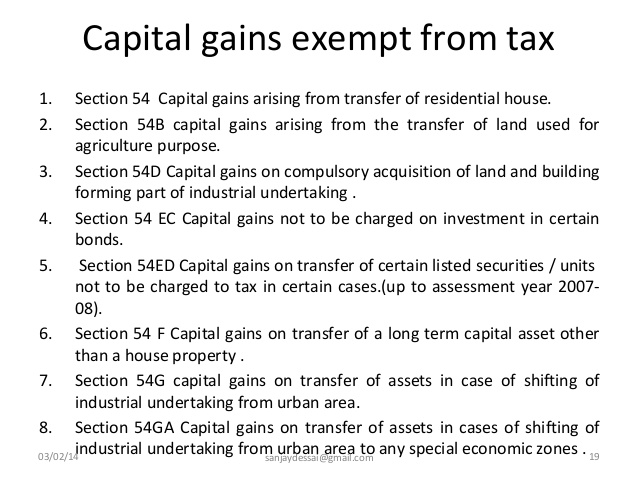

New House is in wife’s Name – Forget about tax-relief from the sale of the house  How can you get tax exemption by selling your asset under Section 54F Income Tax Conditions?

How can you get tax exemption by selling your asset under Section 54F Income Tax Conditions?  Section 80IBA Assures 100% Deduction For Affordable Housing Projects

Section 80IBA Assures 100% Deduction For Affordable Housing Projects  How to Minimize Tax Liability with House Rent Allowance

How to Minimize Tax Liability with House Rent Allowance  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?