Insurance Income: No Escape from Income Tax Surveillance

As per a report in the Business Line, since the beginning of October, a two per cent TDS will be charged on all sums received as insurance income. This is going to be the scene only from certain life insurance policies

However the twist here is that if you have been exempt from paying taxes on all of the sums in the past few days, the picture is going to change. This ensures that all your sums withdrawn as insurance income will indeed be taxable.

In the Budget of 2014-15, the Government introduced a unique provision which allows for taxation from life insurance policy holders in the form of insurance income. It had given high hopes to all the life insurance policy holders, who were not even eligible for tax exemption under the section 10 (10D) that they will be able to see a 2 per cent of tax getting deducted from their source on the total amount to be paid to the policy holder.

This leaves with the policy-decision to be taken by the insurer. The onus is surely on the insurer who will have to deduct TDS on all the mentioned policies where maturity would proceed and would be taxable.

However, the pinching point here is that you tax liability does not end with just a 2 per cent TDs. Income tax payers who are eligible for tax exemption under Section 10 (10D) will still be taxed for their normal insurance income at the stated individual’s slab rate.

The contributions towards a unique life insurance policy become eligible for smooth tax deduction under the Section 80C of the IT Act.

A clue given by Suresh Surana, who is the Founder, RSM Astute Consulting, a tax advisory firm, is that in order to be eligible for tax benefits, the premium amount should not cross the 10 per cent of the sum which is assured in insurance income. If it turns out to be a policy which is issued well before April 1, 2012, then there exist chances of premium amount not crossing 20 per cent of the total amount.

In case, if the total amount of premium is exceeding the limit prescribed above, you would be left to stand to lose the total exemption rate to the extent that it exceeds the limit. Harsh Roongta, who is a well-known CEO of Apnapaisa, says that “It is only a premium that equals around 10 per cent of the sum assured under the stated policy, which will be eligible for complete tax deduction under the given Section 80 C. He further adds that one will not be eligible to claim tax exemption under the tough Section 10 (10D).

Life Insurance Policy Payouts – Are they Taxable or Not?

Life Insurance Policy Payouts – Are they Taxable or Not?  Insurance is a Practical Business Investment

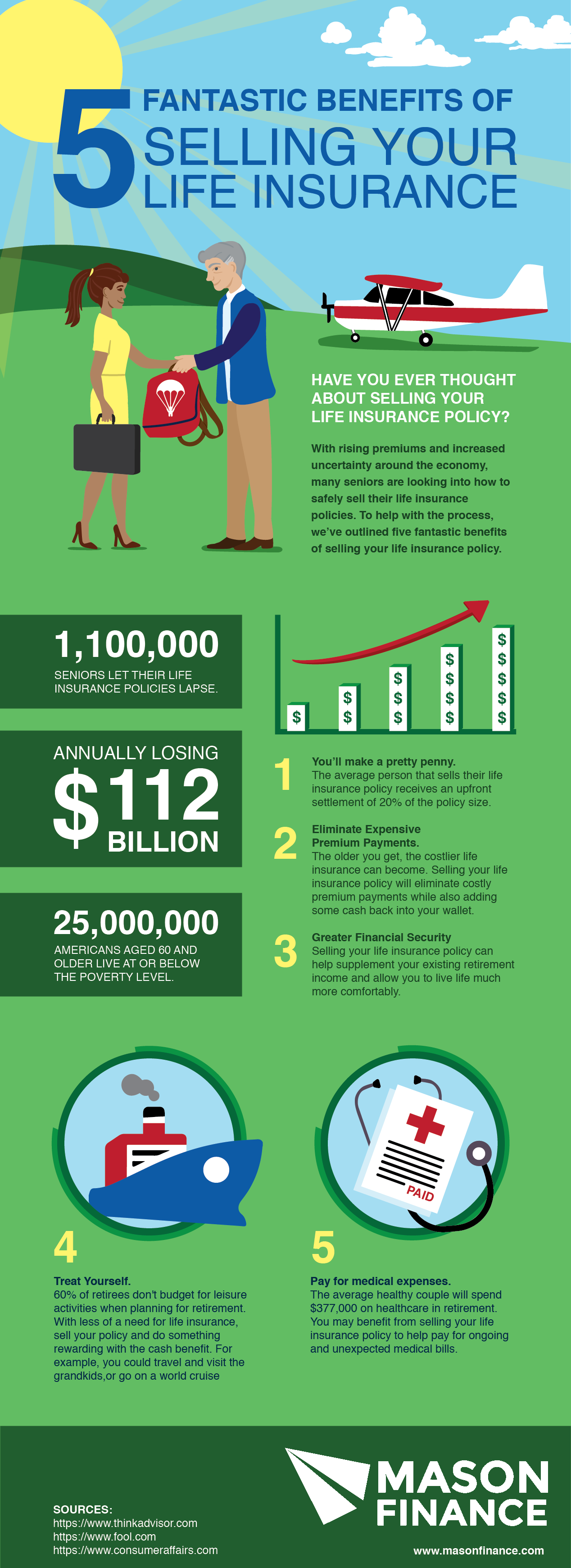

Insurance is a Practical Business Investment  5 fantastic benefits of selling your life insurance

5 fantastic benefits of selling your life insurance  Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?

Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?  Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you

Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you  Life Insurance Policies – Are they really bliss?

Life Insurance Policies – Are they really bliss?  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?