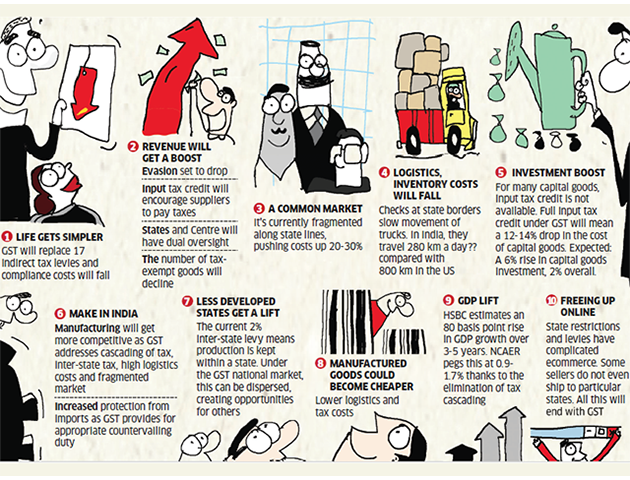

Some important points to be considered under Goods and Service Tax

Forget the hype and hoopla under GST- Come GST and it is likely to increase prices of many goods as well add multiply compliance burden of suppliers

We are passing through the tax regime where complete indirect tax system will switch over to the Goods and Service Tax (GST) which includes four major Acts i.e. IGST, CGST, SGST & UGST. All the four governed acts will work as per their applicability in their respective domains.

What is Taxable Event and Concept of Supply in GST?

It is very significant to understand that under the Goods and Service Tax (GST) taxable event will be the supply of goods or services (or both) in the course of the continuance of business whereas under the current indirect tax structure the taxable events are on manufacturing, on sale or on a rendering of services. It is essential to know the concept of supply in which key terms like a barter system, sale transfer, lease, exchange license and disposal plays very important role.

Certain Essentials in a transaction for GST to be applicable on it

Goods and Service Tax (GST) will be applicable if the transaction meets the below mentioned six requirements:

- The transaction includes supply of goods or services or both,

- The supply is made in the course or continuance of business;

- The supply is made for a consideration unless and until specifically provided for;

- The supply is a taxable under the act,

- The supply is made in the taxable territory; and

- The same supply is made by a taxable person.

When is GST levied?

GST will levy on each and every stage of supply and when the same supply is sold (within the state) then CGST and SGST both will become applicable. For an instance, if the tax rate on a specific item is 18% then the seller of such item is to charge 9% on the invoice as CGST and the reminder 9% as SGST simultaneously.

If it is an interstate sale then the seller of the goods has to charge IGST only on the invoice, though the rate will remain same.

Under Goods and Service and Tax laws, all the registration certificates will be issued through online and dealer is required to upload each and every sale and purchase bill.- Will this make GST any simpler or adding more to already burdened business community with further compliances

The Central Government has issued draft Way (e-way) Bill Rules under the GST Ac – some important provisions are as under:

- The E-way bill is mandatory for goods value exceeding Rs.50000

- The E-way bill will have to be issued via online through GST website

- The E-way bill validity from the time and date of its issuance will be as under:

– for 100 km – 1 day

– for 100 to 300 km – 3 days

– for 300 to 500 km – 5 days

– for 500 to 1000 km – 10 days

– for more than 1000 km – 15 days

Cancellation of e-way bills and detention of Vehicles

- The Cancellation of the E-way bill can be done within 24 hours of its issuance

- Where a vehicle has been detained for more than 30 minutes, the transporter can upload this information on GSTN.

Inspection and Search under GST

- Prior permission of Joint Commissioner (JC) will be required for conducting an inspection and the permission should be on the basis of some reasoning.

- To convert an inspection into a search, a valid search warrant will be required.

- If the officer wants to search a house, then a lady officer must accompany the searching officer.

- There is an obligation on the officer to show his identity.

- Signature of the aggrieved person is mandatory on a search warrant.

- A Proper “Panchnama” is required for the seized stock and records or for accountability,

- Beside the Signature of the person on whose premises search has been conducted, the signature of two witnesses are required.

- Where any document have been impounded, then the same must be returned back to the concerned person within a period of 60 days.

Export of Goods under GST

- Every dealer who is eligible for the refund will get 90 percent of the total amount as the refund within 7 days’ time.

- In other instances, if the dealer wants a 100% refund in totality then the department is under an onus to grant the same within a period of 60 days.

The Commissioner has empowered to make the installments of the tax due where the dealer satisfies his financial hardship.

Assessment of Sales and Purchases under GST

Apart from the scrutiny self-assessment, provisional assessment, summary assessment, regular assessment, a new concept of protective assessment has been inserted as prevalent under the Income Tax Act.

Normal Time limit for completing the assessment is 3 years but in the cases of fraud or any willful statement of suppression of the facts or evasion of tax then the period can be extended to five years.

Treatment of Goods returned under GST System

As per the provisions of the act when buyer returns the goods to the supplier then supplier is under a compulsion to issue the credit note to the purchaser and both the transactions are should be shown on the returns so that the credit note details shall be matched with the parallel reduction in claim for input tax credit by the buyer in his valid tax return for the same tax period or in any subsequent period and concurrently the decrease in output tax liability by the supplier.

Wrapping up- Would GST help business Community or Burden it further making business even more tougher

It is undoubted that the Goods and Service Tax Act is the Act which consists number of other indirect taxes which are working altogether for the collection of the indirect taxes, duties etc. like (a) Central Sales Tax, (b) Service Tax, (c) Value Added Tax (VAT), (d) Central Excise Duty, (e) Purchase Tax, (f)Luxury Tax, (g) Entry Tax (h)Lottery Tax, (i) Entertainment Tax, (j) Cess and Surcharge, (k) Additional Duty of Custom (CVD), (l) Special Additional Duty of Custom (SAD) (m) Additional Duty of Excise and the effort is to lessen the problems of the dealers as the Government has finalized to take-off the check posts and only mobile check posts will be enforce everything and will be online.

However complexity of the returns and rigity of the system may act as spoiler and a small or medium business man may find it difficult to ensure all compliances

Related Read- Some Common Queries about GST

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know  What Is The GST Liability on Free Supply of Goods and Services?

What Is The GST Liability on Free Supply of Goods and Services?  Some FAQs about GST- Understanding Scope and Provisions of GST

Some FAQs about GST- Understanding Scope and Provisions of GST  Understanding the Reverse Charge mechanism under GST and IGST?

Understanding the Reverse Charge mechanism under GST and IGST?  Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?

Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?  Arrests and Detention Provisions under GST in Detail- Are these justified

Arrests and Detention Provisions under GST in Detail- Are these justified  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?