Understanding the Reverse Charge mechanism under GST and IGST?

Impact of reverse charge mechanism under GST and factors to be considered

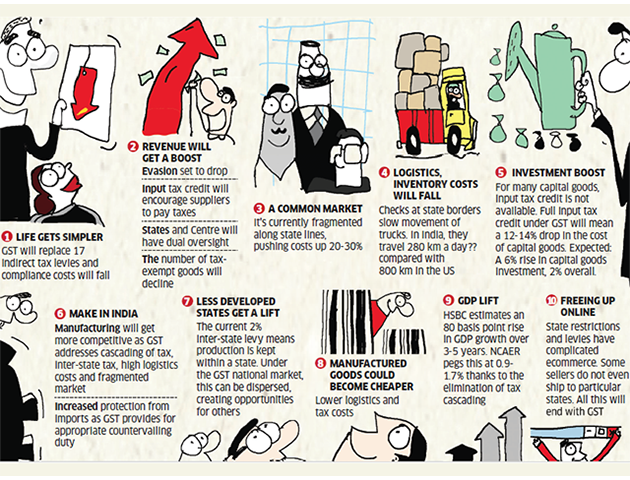

The Goods and Services Act, 2017, has perhaps been one of the long vision steps taken by the government of India. It came with an array of implementation and inclusions. One such inclusion is the concept of reverse charge in GST. To any Service Tax Payer, the concepts of Complete Reverse Charge or Partial Reverse Charge are nothing new. Popularly known as RCM and PRCM, respectively, they were inducted under the Finance Act, 1994. As this proved to be a success, the present government has decided to extend this concept to the Goods and covered unauthorized business sector, under the new GST Act. As 1st July is nearing, it is essential to have a clear idea of what is going to be implemented.

There are mainly two impacts of the reverse charge that will affect the people. They are:

-

The First Type of Reverse Charge: Specified goods or services notified by the government under GST Act

The Section 9(3) of the CGST Act, 2017 (with similar provisions under Integrated Goods and Services Tax Act and SGST Act as well), gives government the power to notify, on the recommendations of the Council, the categories of supply of goods or services or both, the tax on which shall be paid on the basis of reverse charge by the recipient of such goods or services or both and the recipient is open to all the provisions of this act as if he/she is the person who is liable to pay the tax in relation to such goods or services or both.

-

The Second Type of Reverse Charge: Mandatory on supplies from unregistered to registered person

This falls under the Section 9(4) of GST Act, 2017, and it almost threatens to kill the small businesses as it lays down a very straightforward provision saying that tax on taxable goods or services, which excludes non-exempt services or nil rated goods, shall be paid by recipients if the supplier is not registered under GST, however, the recipient is entitled to input credits of such taxes.

This exempt will fail to save small businesses as it makes the supply of goods from unregistered suppliers to registered suppliers, difficult. Several e-commerce sites have come out saying that they will not provide their platform to sell goods if the supplier is not registered.

There have been some other conditions levied on the situation of registered and unregistered recipients in Section 5(4) of the Integrated Goods and Services Tax Act. The section of the IGST Act or the Integrated Goods and Services Tax Act says that, on the supply of goods and services or both provided by a non-registered to a registered person in course of an interstate trade, the tax shall be paid by the recipient. However, under Section 24 of the GST Act, it is mandatory to be registered for an inter-state trade.

Apart from these important impacts of reverse charge, there are some others as well

- Significant changes will have to be done in accounting of Sales and Purchases.

- Tax invoices will have to be prepared for the reverse charge. These Invoices can be prepared now once a month as against earlier proposal of invoice against each purchase

- The RCM tax will have to be paid as due, and would not be able to get adjusted against any adjustments available in balance.

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know  What Is The GST Liability on Free Supply of Goods and Services?

What Is The GST Liability on Free Supply of Goods and Services?  Some FAQs about GST- Understanding Scope and Provisions of GST

Some FAQs about GST- Understanding Scope and Provisions of GST  Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?

Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?  Arrests and Detention Provisions under GST in Detail- Are these justified

Arrests and Detention Provisions under GST in Detail- Are these justified  Some important points to be considered under Goods and Service Tax

Some important points to be considered under Goods and Service Tax  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?