Arrests and Detention Provisions under GST in Detail- Are these justified

Arrests and Detention Provisions under GST- Are such Harsh Measures justified?

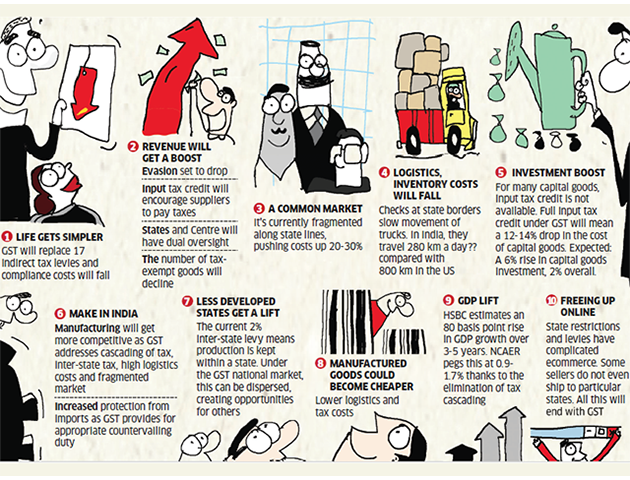

The Goods and Services Tax will be applicable all over India from the 1st of July this year. There are many dealers, whether big or small who are going to get affected by it. It is a major transformation from the indirect system of taxation being replaced by the GST. Lets read the Provisions under GST. Of course, this change is inevitable, but it is the human nature to resist any change since one fears change. Here we talk about the Arrest that can take place under the GST. It has to be understood that Arrest denotes a serious action and one is bound to get skeptical and be anxious about such a change.

Arrests and Detention Provisions under GST

Arrest and detention under GST provisions

If a person is guilty of committing an offense under Section 132 found by the Commissioner of CGST or SGST, then the arresting officer will be authorized by the commissioner, and he will have the last word. The person who is arrested will be given the basis of his detention in writing.

Offenses under section 132 of GST Act with applicable detention provisions

- These are the offenses in which the arrest provisions become applicable:

- In case a person gives goods or services without issuing any invoice of the same or if the issued invoice is false since he intends to evade tax.

- In case a person collects GST but due to some reason, does not submit it to the government within a period of 3 months.

- He issues a bill or an invoice without supplying goods or services. It is a violation of the provisions of the GST that can lead to wrongfully availed input credit or the refund of tax.

In all of these cases, there is an evasion of tax.

Cognizable and Non- cognizable Offences that yo may run in- in GST Act

The cognizable offense in GST means a crime that is linked to goods and services that are taxable. The amount of input credit, tax evasion or the refund may be wrongly construed and can amount to Rs 5 Crores or more than that. The cognizable offenses are non-bailable.

The cognizable offense is such in which the police is capable of arresting a person even if they do not have an arrest warrant. Their crimes and offenses are serious. On the other hand, the non-cognizable offenses are those in which police are not authorized to arrest a person without any warrant and that too, has to be issued by some competent authority. These crimes and offenses are less serious than the cognizable ones.

Commission can arrest a person suspecting him of evading GST even without a warrant

The Commissioner has all the discretion in the decision to arrest a person in the case of fraud of GST. The power that the Commissioner has must be used carefully. There must be a careful investigation before making the arrest, avoidance of tampering with evidence, prevent the influence of witnesses and also ensure that the offender doesn’t go absconding after committing the offense.

GST is a new law in the arena of Trade and Industry, and there are apprehensions whenever anything new is introduced. The powers that come with GST can also be misused. Therefore, there is a need for careful interpretation and inoculation of this law so as not to lead to any problems in the future.

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know

Sales Tax For E-Commerce: 3 Things Small Businesses Should Know  What Is The GST Liability on Free Supply of Goods and Services?

What Is The GST Liability on Free Supply of Goods and Services?  Some FAQs about GST- Understanding Scope and Provisions of GST

Some FAQs about GST- Understanding Scope and Provisions of GST  Understanding the Reverse Charge mechanism under GST and IGST?

Understanding the Reverse Charge mechanism under GST and IGST?  Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?

Pros and Cons of GST- Is Ushering in of GST worth Celebrating as media wants us to believe?  Some important points to be considered under Goods and Service Tax

Some important points to be considered under Goods and Service Tax  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?